Property Purchase Translation UK: The Documents Buyers Most Often Miss

Buying property is stressful enough without a last-minute request for translated paperwork. In many UK transactions, the issue is not whether a buyer can prove identity or funds at all. It is whether the supporting documents are complete, readable, consistent, and usable by the estate agent, conveyancer, lender, or compliance team reviewing them. Buyers often focus on the headline document they expect to be asked for, then lose time because the supporting trail is still in another language. Estate agents, lawyers, and mortgage lenders may all ask for identity, address, and source-of-funds evidence during the purchase journey.

That is why property purchase translation in the UK is rarely just about one mortgage paper or one deed. It is usually about a pack of related documents that need to make sense together. A better way to think about it is this: do not translate single pages in isolation. Translate document families.

Why buyers get delayed even after sending “the main document”

A property file can look complete at first glance and still trigger follow-up questions. A buyer may send:

- a bank statement showing the balance

- a passport copy

- a signed mortgage offer

But the reviewer may still need:

- the earlier statement showing where the funds came from

- the sale agreement for the property that generated the money

- a gift letter from a family member

- a marriage certificate explaining a surname difference

- a power of attorney if someone else is signing

- company ownership documents if the purchase is not in a personal name

This is where delays begin. The missing item is often not the obvious one. It is the supporting document behind the supporting document. The fastest property purchase files are usually not the shortest. They are the clearest.

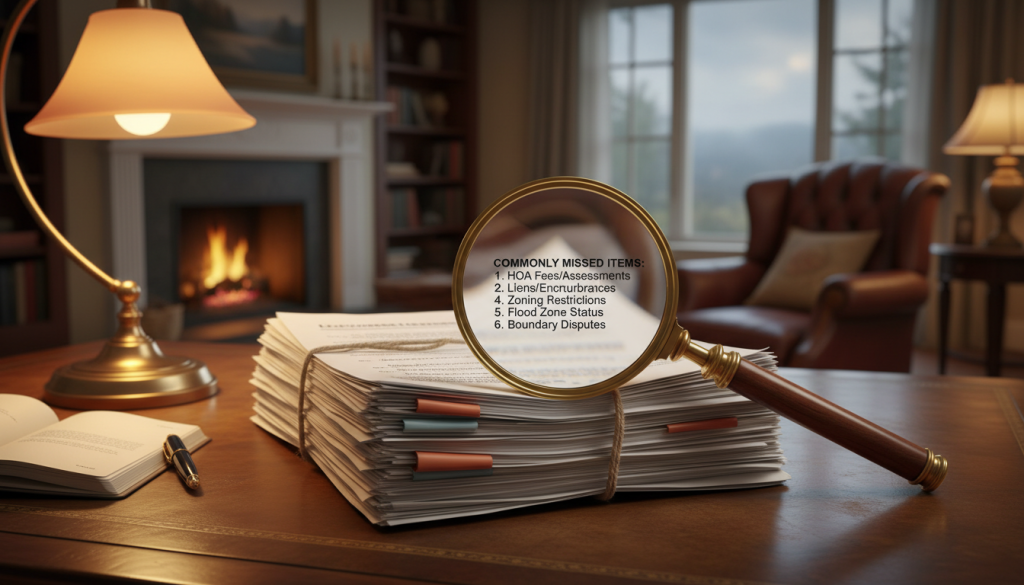

The documents people miss most in a UK property purchase

1. Proof of funds is a trail, not a single document

This is the biggest gap in most files. Buyers often assume a recent bank statement will be enough. Sometimes it is the starting point, but not the whole story. A property team may want to understand where the purchase money came from, not only where it is sitting today. UK guidance distinguishes source of funds from source of wealth, and that distinction often shapes the paperwork a buyer is asked to provide.

Common proof-of-funds documents that may need certified translation include:

- bank statements

- savings account statements

- fixed deposit certificates

- investment liquidation records

- sale agreements and completion statements from a previous property sale

- inheritance papers

- probate documents

- gift letters

- dividend statements

- share sale records

- tax returns or tax assessments

- loan agreements if part of the purchase money is borrowed privately

What buyers miss here

They translate the latest balance statement but not:

- the earlier statement showing the incoming transfer

- the sale contract that explains the transfer

- the notarial deed or completion statement from the overseas sale

- the gift declaration from the family member

- the inheritance record that explains a lump sum

If your conveyancer is trying to follow a money trail, partial translation usually creates more questions, not fewer.

2. Mortgage documents are only one part of the lender pack

Many buyers search for mortgage document translation and stop there. In practice, the lender or broker may need more than the mortgage offer itself. Depending on your case, the pack may also include:

- foreign-language payslips

- employment letters

- tax filings

- bonus letters

- rental income statements

- business accounts

- accountant letters

- existing mortgage statements from another country

- debt schedules

- property valuation reports for overseas assets

For self-employed buyers and overseas buyers, these files often come from more than one institution and more than one jurisdiction. That means names, dates, decimal separators, stamps, and legal wording all need to be rendered clearly and consistently.

3. Deeds, contracts, and ownership records are often left until too late

If part of your purchase money comes from selling another property abroad, or if ownership has to be evidenced through overseas records, title-related paperwork may also need translation. This can include:

- title deeds

- land registry extracts

- purchase contracts

- sale contracts

- notarial transfer deeds

- completion statements

- mortgage discharge papers

- cadastral records

- lease agreements

- occupancy certificates

These documents matter because they explain ownership history, sale proceeds, encumbrances, or legal authority. When they are left untranslated, the reviewer may understand the bank movement but not the event behind it.

The overlooked category: authority to sign

One of the easiest ways to stall a transaction is to forget the document that proves who is allowed to act.

4. Power of attorney documents

If a buyer or seller is abroad, travelling, elderly, or unavailable for signing, a power of attorney may be involved. If that document is in another language, it may need translation alongside any supporting ID or certification attached to it. This is especially important where:

- one family member signs for another

- a corporate officer signs on behalf of a company

- an attorney signs at completion

- a representative handles a sale from overseas

HM Land Registry guidance shows that identity evidence can also become relevant where attorneys are involved, and extra identity evidence may be requested in some cases to reduce registration fraud risk.

5. Board resolutions and company authority documents

When the buyer is not an individual, the document set becomes wider very quickly. Common company-related documents that may need certified translation include:

- certificate of incorporation

- articles of association

- commercial register extracts

- shareholder registers

- beneficial ownership records

- board resolutions approving the purchase

- signing authority certificates

- constitutional documents

- trust-related paperwork where relevant

For overseas entities buying or dealing with UK property, Companies House and HM Land Registry guidance around the Register of Overseas Entities can become relevant too.

The quiet problem no one notices at first: name mismatches

A translation can be accurate and still fail to help if the file does not explain why one person appears under different names.

6. Marriage, divorce, and name-change records

These are often missed because they do not feel like property documents. But they are frequently the missing bridge between two otherwise valid records. Examples include:

- the passport is in a maiden name, but the bank account is in a married name

- the gift donor’s surname differs from the buyer’s current documents

- the sale agreement uses an older spelling

- an overseas document uses a patronymic or transliterated variant

- a company officer’s name is shown one way in the passport and another way in the register

In those cases, supporting records may need translation too:

- marriage certificates

- divorce decrees

- change-of-name certificates

- deed polls

- civil status records

A strong file does not merely translate words. It removes preventable doubt.

What a certified translation should do in property matters

For property purchase translation in the UK, the goal is not decorative formatting. It is traceability. A strong certified translation should help the reviewer match:

- names

- dates

- addresses

- reference numbers

- account numbers

- clause headings

- signatures

- seals

- stamps

- annotations

- page order

It should also preserve the structure of the original where that structure helps the reviewer understand the document. That matters especially for:

- bank statements with multi-page transaction histories

- deeds with marginal notes or seals

- contracts with initials on each page

- bilingual forms with handwritten notes

- documents carrying registry stamps or notarial marks

What should be included

Where certified translation is requested, buyers should expect a complete translation accompanied by a certification statement that confirms the translation is accurate, along with the translator or company details needed for official use.

A simple rule that saves time: send the whole pack at once

One of the most expensive mistakes in property purchase translation is ordering one document at a time as new requests come in. That approach creates three problems:

- inconsistent formatting across files

- repeated rush fees

- missing cross-references between related documents

A better handover looks like this:

Send these together where possible

- the document you were directly asked for

- the supporting document that explains it

- the ID document that matches the person named in it

- any document explaining a name change

- any covering email or checklist from your solicitor or lender showing what they want

Tell the translator these details upfront

- who will review the translation

- whether the file is for a lender, solicitor, broker, or registry-related purpose

- whether hard copies may be needed later

- whether signatures, stamps, and handwritten notes must be described

- whether there is a deadline tied to exchange or completion

That one step often turns a reactive order into a clean, usable file.

Property transactions have multiple reviewers, not one

Another reason buyers underestimate translation needs is that they assume one acceptance decision covers everything. In reality, a purchase can involve separate checks by:

- the estate agent

- the mortgage broker

- the lender

- the conveyancer

- the compliance team

- the Land Registry process in certain circumstances

Government guidance aimed at homebuyers makes clear that identity and source-of-funds checks can arise at several stages of the transaction, not just once. That means a document translated only to satisfy one reviewer may still leave gaps for the next.

Three real-world scenarios that explain why documents get missed

Scenario 1: Sale proceeds from abroad

A buyer provides a translated bank statement showing £180,000 in savings. The conveyancer then asks where the funds came from. The buyer now has to add:

- the overseas sale agreement

- the completion statement

- the land record

- the mortgage discharge

- the statement showing the incoming transfer

The delay was not caused by the bank statement. It was caused by the missing chain behind it.

Scenario 2: Joint buyers with different surnames

A couple are purchasing together. One passport is in a current surname, but the source account is in a former surname. The file now needs:

- the bank statement

- the passport

- the marriage certificate or name-change record

Again, the problem is not the main file. It is the missing bridge.

Scenario 3: Company buyer from overseas

The buyer is a foreign company purchasing through a director. The solicitor may ask for:

- company formation documents

- register extracts

- beneficial owner information

- board resolution

- director ID

- proof of funds documents

- authority to sign

This is where corporate property purchase translation UK work becomes a bundled legal-and-financial job rather than a single-document request.

When to order your translations

The best moment is usually before the formal chase begins. Order early if any of the following are true:

- your purchase money comes from outside the UK

- your documents are spread across more than one country

- your legal name has changed

- a family gift forms part of the deposit

- a power of attorney is involved

- a company, trust, or overseas entity is purchasing

- your proof-of-funds history runs across several months or institutions

Waiting until the week of exchange is rarely the cheapest or calmest route.

A practical checklist before you upload your files

Before sending anything for translation, check that you have:

- Full-page scans, not cropped screenshots

- Every page, including backs if stamped or annotated

- Related documents grouped together

- Name-bridge documents included

- Clear indication of which documents support source of funds

- Any solicitor or lender request email saved as reference

- Confirmation of whether you need digital delivery only or may later want hard copies

If you can assemble that pack before your conveyancer has to chase you twice, you are already ahead of most buyers.

Why buyers choose a specialist provider instead of general translation

Property purchases combine legal wording, financial terminology, identity checks, and deadline pressure. That mix is why buyers usually do better with a provider used to certified legal and financial files rather than a general text-only translation workflow. 24 Hour Translation positions its service around legal, financial, and certified document work, with secure handling, official-document support, and fast turnaround processes for sensitive files. If your purchase depends on a clean proof-of-funds trail, a readable deed, or authority documents that must line up across multiple parties, it is worth getting the whole pack reviewed together before it holds up exchange or completion.

Send the full set, not just the page you were first asked for, and get the translation done while there is still room to fix follow-up requests calmly.

FAQ Section

Do I need certified translation for proof of funds in a UK property purchase?

If your proof-of-funds documents are not in English, certified translation is commonly requested so the reviewer can understand the origin of the money clearly and keep a usable compliance record. This often applies to bank statements, sale proceeds documents, inheritance papers, and gift letters.

Can I translate only the summary page of my bank statements?

Sometimes a summary page is not enough. If the reviewer needs to trace where the money came from, they may also need earlier pages, incoming transfer details, and the document that explains the transaction behind that transfer. For property purchase translation UK work, the full trail is often more important than the headline balance.

Do deed and contract documents need certified translation in a property purchase?

They can. If a deed, sale contract, land extract, or completion statement is being used to evidence ownership, sale proceeds, or legal authority, it should usually be translated in a form the solicitor or compliance reviewer can rely on.

Do I need to translate power of attorney documents for a property purchase?

Yes, if the power of attorney is in another language and is part of the signing or authority chain. Supporting ID or related authority documents may also be needed, especially where attorney identity evidence becomes relevant in the transaction.

What company documents may need translation when buying UK property?

For company or overseas-entity purchases, the file may include incorporation documents, register extracts, articles, beneficial ownership records, and board resolutions, alongside proof-of-funds paperwork. Overseas entities dealing with UK property may also need to consider Register of Overseas Entities requirements.

Will a digital certified translation be enough?

Often yes for the first review stage, but some transactions may later require hard copies or additional formalities depending on who is reviewing the file. It is best to confirm this before completion week so your translation package matches the use case from the start.